Summary

- Dividend investing may seem simple in theory, but there are many pitfalls that investors fall into along the journey.

- I share perhaps the biggest mistake that many dividend investors are making in the current market environment.

- I share how to avoid it, along with some areas of the market I am finding a lot of attractive opportunities right now.

- Looking for a portfolio of ideas like this one? Members of High Yield Investor get exclusive access to our subscriber-only portfolios. Learn More »

Recently, a reader commented to me that this is a “momentum market,” in which, in order to achieve attractive performance, it is important to invest where the market has positive sentiment and shun sectors that are out of favor. While this can work well at times, it ultimately amounts to chasing the hot stocks and sectors.

What this puts you at risk of doing is buying high and potentially near the top, thereby providing exit liquidity for those who bought stocks and sectors when they were truly attractive values. Thus, if your timing is not perfect and the market suddenly turns against you, you could end up sitting on massive losses and having to wait a long time to get out at breakeven.

In contrast, investors who are guided purely by the valuation and fundamentals of what they buy do not have to time their investments perfectly. Instead, they can actually let time be their friend by allowing the wealth of their underlying holdings to grow until the sector and/or stock moves back into favor. At that point, there should be a massive catch-up of market sentiment relative to fundamentals, thereby leading to outsized long-term total returns with much less timing risk.

Thus, I think that one of the biggest mistakes that dividend investors are making right now is allowing the current highly bifurcated market and momentum-driven investing sentiment to cause them to abandon their core investing principles. This puts them at risk of a painful long-term setback to their income and wealth compounding. In this article, I will detail more about this issue and how investors can avoid it.

When Momentum Turns Into A Painful Reversal

The danger of momentum investing was most recently demonstrated by the significant volatility driven by the Iran war, with oil-related stocks (XLE

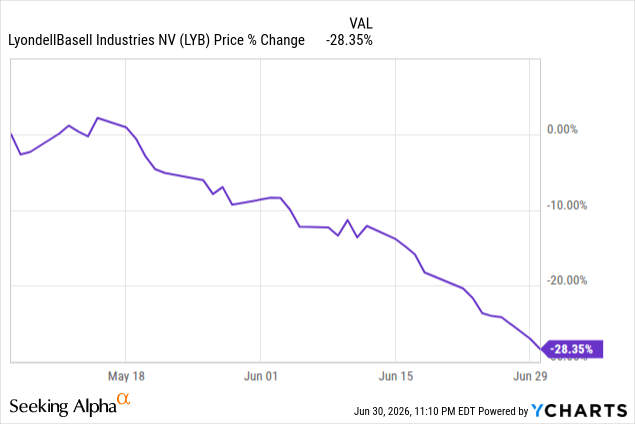

This means that investors who chased the momentum higher have potentially gotten hammered by buying near the peaks. A classic example of this recent situation is LYB, which was rated one of the leading momentum stocks near its highs, so investors who followed that momentum indicator likely got burned on LYB as it crashed hard after:

Of course, there are plenty of examples where momentum pays off, as it has with many AI stocks thus far. This is simply a cautionary warning that momentum is not a guaranteed winning indicator and that when you’re wrong, it often leads to steep losses and a very uncertain time frame from which to recoup those losses.

Why Value Investing Rewards Patience

This contrasts with value investing, even in names that are out of favor and can continue dropping, with a recent example for me being Blue Owl Capital (OWL

In the case of OWL, its AUM is continuing to grow, along with its distributable earnings and ultimately its dividends. Therefore, eventually, once market sentiment shifts, the stock price should see a significant snapback higher, as has been commonly seen in the alternative asset management space, including what recently happened with Blackstone (BX

The Playbook For Navigating A Bifurcated Market

So how should investors approach these investments? In particular, what should they focus on with dividend stocks?

First and foremost, it is essential to buy quality dividend stocks that have a likelihood of continuing to compound their underlying intrinsic value over time. The reason this is important is that even if the market remains unfavorable towards that stock and/or sector for a prolonged period of time, the underlying intrinsic value continues to compound. Therefore, the time frame of having to hold it means little, since your intrinsic value continues to compound anyway. In contrast, if you’re buying a lower-quality company, especially one that is in decline, the longer you have to hold the stock, the worse off you’re going to be, because the intrinsic value of the business continues to decline over time, thereby leading to a weaker recovery if and/or when that sector and stock receive a more favorable appraisal from Mr. Market. As Warren Buffett once said:

Time is the friend of the wonderful company, the enemy of the mediocre.

Additionally, ensuring that your valuation estimates are conservative from the get-go is highly important too, because this way, if unfortunate events pop up and/or the market was pricing in something that you did not fully appreciate the risks of when you made the initial investment, you have some margin of safety that helps protect you from long-term permanent losses. OWL is a great example of this as well, because its growth rate has slowed considerably due to souring market sentiment on direct lending, which is about one-third of its total AUM. Thus, its perceived intrinsic value today is materially lower than it was even just a year or two ago because of the weakening growth outlook for the company, at least in the near term.

As a result, if you underwrote the valuation at a material margin of safety, it would have already baked in some of that weakening growth, and therefore your intrinsic value estimate at which you underwrote the investment originally would likely not be too far from where it is today in reality. Therefore, you can still be confident that by holding the stock over time, you’re more likely than not to eventually get back to breakeven and even make a profit, even if you had bought it a year or a year and a half ago when the stock price was much higher than it is today.

Another important attribute is to ensure that you diversify intelligently across sectors. That way, if one or two sectors suddenly fall out of favor, your aggregate portfolio performance will likely still be decent across different market conditions. While this helps psychologically at a minimum, it can also help enhance long-term total returns by giving you one favored sector from which you can recycle capital into other sectors that are more out of favor. This happened recently to me, where my BDC (BIZD

Don’t Get Burned Playing The Scoreboard Game

Last but not least, patience and being focused on the playing field rather than the scoreboard are what will separate the long-term winners from the speculators and momentum chasers. As Warren Buffett once said,

Games are won by players who focus on the playing field – not by those whose eyes are glued to the scoreboard.

Ultimately, momentum chasers are scoreboard watchers, whereas value investors are focused on the playing field. Those buying into many hot AI stocks at today’s elevated valuations are, in my opinion, playing with fire by risking significantly overpaying for some of these companies and therefore being stuck with heavy losses that are unlikely to be recouped anytime soon if they’re still holding the stocks when the momentum shifts against the sector. Likewise, those who piled into oil stocks after they and related beneficiaries of the Strait of Hormuz closure had already established themselves as significantly strong momentum stocks have since incurred heavy losses on the sharp pullback.

Therefore, I think dividend investors need to be patient and fight the fear of missing out and the urge to try to chase momentum, and instead remain focused on the playing field by putting a high priority on fundamental and valuation analysis, and then letting time in the market, rather than trying to time sectors and stocks, do the work for them. This is the approach that we are taking in our 7-8% yielding total return outperforming and below-market-beta portfolios at High-Yield Investor. In particular, we are finding a lot of opportunities in high-quality, yet out-of-favor, infrastructure companies (UTF