Summary

- Schwab U.S. Dividend Equity ETF faces near-term headwinds from rising interest rates and renewed investor preference for growth and AI-driven stocks.

- Persistently high rates make SCHD’s dividend yield less attractive versus risk-free treasuries, leading to potential further drawdowns and underperformance versus the broader market.

- While SCHD remains a long-term income and capital appreciation vehicle, current market conditions favor trimming or waiting for a 10%+ drawdown before adding.

- Diversification in SCHD’s top blue-chip holdings mitigates single-stock risk, but macro pressures and Fed policy may drive further near-term weakness.

- Looking for a helping hand in the market? Members of BAD BEAT Investing get exclusive ideas and guidance to navigate any climate. Learn More »

- Sitewide Sale 2026: Get 20% Off

Well, the tides are starting to turn for the Schwab U.S. Dividend Equity ETF (SCHD

We believe that conditions have changed somewhat that will take dividend stocks out of favor again for the foreseeable future relative to the broader market. In general, over the last 5 years, SCHD indeed lagged the market. This is all mostly due to investors favoring growth and the AI revolution. It also performed badly as interest rates started to rise. We are seeing interest rates rise again. And if you saw the Fed statement and press conference yesterday, then that is a big clue that we may be dealing with higher-for-longer interest rates.

Higher-for-longer interest rates are not good for SCHD. This is because it holds dividend payers. And dividend-paying stocks become extra risky for investors compared to buying simple treasuries and bond funds. Why invest for 3-3.5% with stock risk when a two-year treasury could net you over 4% with almost no risk? Even a one month is about 3.65% annualized. Other bond funds with minimal risk pay over that amount in a year. With yields on the rise, investors will shy away from dividend stocks, and by extension, you see the dumping off of SCHD.

Not only does SCHD struggle to keep pace during massive tech-led bull runs, which we are seeing again, but now we have the issue of a more hawkish Fed and the fact that rates are going to remain elevated. Long-term, can you take advantage of prolonged weakness? Yes, you can. If you are an investor focused on risk management and consistent dividend growth, SCHD will provide that (long-term). But you have to pick your spots. If you look back to our history of buy calls, it was all when SCHD was weak. We became more neutral after the huge rally this year. This was because the Iran war was triggering inflation, as evidenced by CPI or PPI data recently.

As such, we are near-term bearish on SCHD. For the long-term investor, this may not matter at all. For those that like to get in and out, SCHD is likely heading lower as rates are persistently high. When rates cool off, SCHD is very likely to do better. But that is not the situation we are in right now. While the end to the Iran conflict should ease inflation some (thanks to lower energy prices and probably lower input costs everywhere else), that is going to take time.

The new Fed Chair was quite pointed, asserting that they will get the job done on price stability. Considering inflation is so high, prices are not stable. Not as bad as a few years ago, but inflation is rearing its ugly head again. The solution to beating inflation is higher rates. This is why two rate hikes are now the odds on favorite this year. It is also why stocks sold off sharply following the Fed decision and press conference. There is some rebound in the averages at the time of this writing, but SCHD is down.

We do not pen this column to instill fear to deter you from investing in great dividend-paying companies or even dividend-paying ETFs like SCHD, which we own and is one of our favorites. But we did shave the position. We will look to redeploy that capital elsewhere. The decision was easy because our cost basis was so much lower than today’s trading price at $31.83.

Why Trimming May Be A Mistake

Now, to balance out the short-term bear take we have right now, we do know that the ETF absolutely continues to deliver safe income and long-term capital appreciation. Near-term, the dividend, of course, is not going anywhere, but there is, for the reasons mentioned above, likely to be negative pressure to persist for a few months. Typically we view SCHD as a solid buy-and-hold candidate. But we even said in our last coverage that buying on a 10% or more drawdown may be a better idea. This market looks like it wants to give it to us.

We also know that if you are trimming our outright liquidation positions, it triggers immediate capital gains taxes in taxable accounts and locks in losses during market pullbacks if you are down. Would find it hard to be down in SCHD right now unless your timing had been horrible. As mentioned, missing a dividend by selling disrupts the compounding of a lower initial cost basis (that is, reinvestments at lower prices).

Another risk is that when you look at the individual holdings, the concentration in top-tier blue chips remains a key feature that helps mitigate single-stock risk. High rates can also hurt growth names; we want to be clear. While not often enough to disrupt mega caps or large caps, we do see higher rates hitting smaller caps. That is not a risk for SCHD given its holdings. Further, while we stand by the assertion that higher rates will deter dividend buyers, the diversification in the top holdings could limit any dumping off of SCHD.

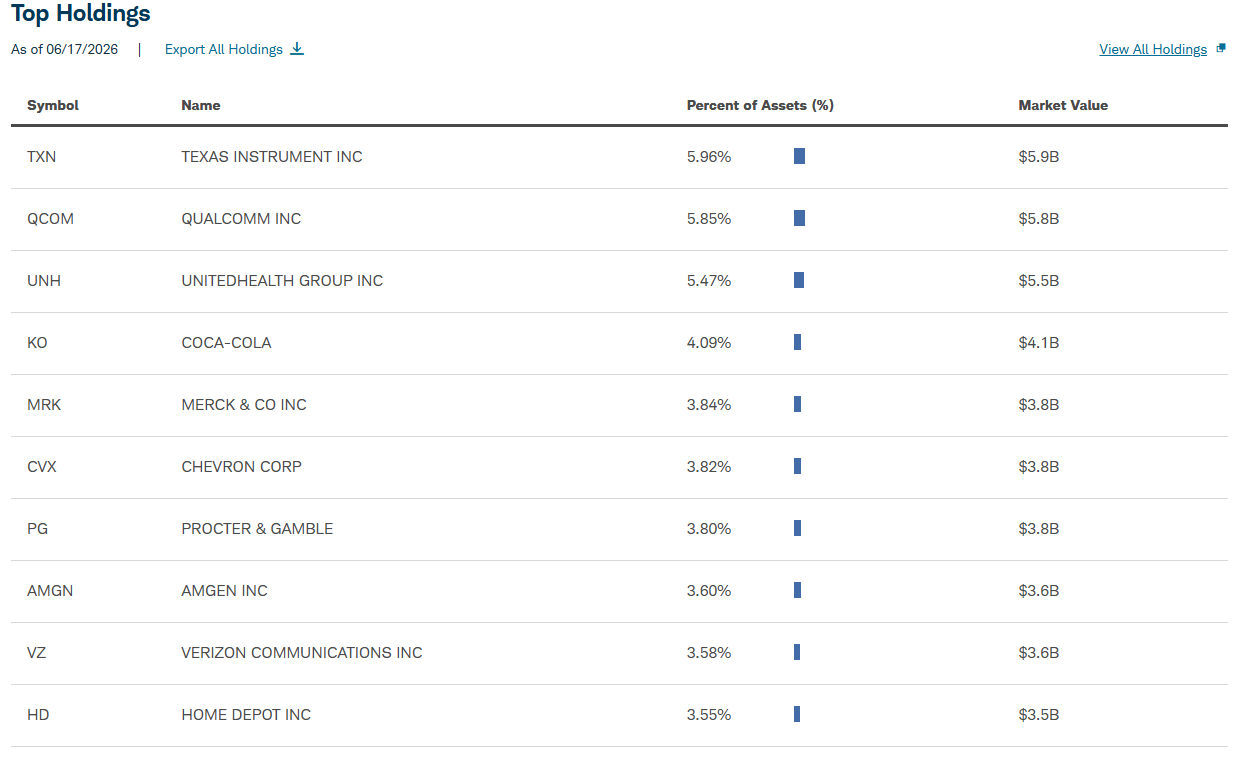

As you can see here, Texas Instruments Incorporated (TXN

Overall, we think you will see some dumping off of SCHD further in the coming weeks and months. While SCHD has diversification as some protection during macro carnage, dividend payers fall out of favor when rates rise dramatically. If the Fed does hike rates, we think it will mean more downside for SCHD, similar to what we saw a few years ago. If you are a long-term investor and are taking a dollar-cost average approach, then it may not matter much to you. However, the reasons for what we see as more declines from here are due to both tech strength and rates.