Summary

- A long-trusted strategy is suddenly breaking down in ways few anticipated.

- Yields are rising, but the real danger is lurking beneath the surface.

- The safest dividend names may no longer be what investors think.

Dividend growth investors tend to think long term, and for years, multinational dividend growth stocks like PepsiCo (PEP

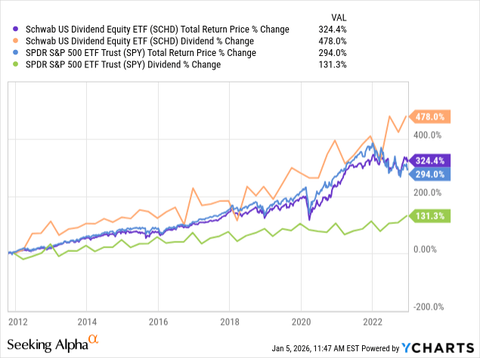

In fact, a simplified approach to dividend investing could simply be to just buy the Schwab U.S. Dividend Equity ETF (SCHD

However, the last couple of years have been quite disappointing for these stocks, as evidenced by SCHD’s abysmal underperformance:

The consumer goods sector (VDC

In this article, we will look at why this is and what the implications are for dividend growth investors moving forward.

Why Dividend Growth Stocks Are Struggling

The biggest problem facing dividend growth stocks today is the fact that they are facing considerable structural pressure on two sides. On the one hand, they are facing tariff-related pressures, while on the other side, they are still battling persistent inflation and a weakening consumer.

As a result, they can no longer pass on all of their higher costs to consumers, as they have previously, and therefore, the pricing power that traditionally funded their strong dividend growth and drove their strong stock price appreciation is now declining.

As margins are compressing, free cash flows are under pressure. Ultimately, their dividend growth is slowing, and in some cases, such as with Conagra Brands (CAG

There are other companies like United Parcel Service (UPS

Thus, what were previously steady-eddy, very safe dividend growth machines are now becoming increasingly risky.

Tariffs, Inflation, and a Weaker Consumer

Tariffs have been a somewhat surprising hit over the past year, because previously there was a general assumption that we were in a globalized economy where tariffs were likely to remain low and only would be placed on very niche and select items as tools for protecting very specific national security essential industries and/or to effectively sanction a certain country.

However, the Trump administration’s approach to tariffs has been much broader and more sweeping in nature, and as a result, it has forced many companies to absorb at least some of the costs of these tariffs to retain market share and keep flagging consumer demand from completely vanishing.

This is especially important given that debt levels in United States households are at record levels, with credit card debt in particular reaching troublesome levels, and consumer sentiment at a very weak level as well.

In fact, it is only the wealthiest consumers who are propping up consumer demand, which means that the broad-based demand that many of these multinational corporations depend on to drive strong volumes in their sales is weakening.

Moreover, many companies have already reported the impacts that tariffs are having on their bottom lines. For example, PG has a projected $1 billion hit from tariff-related costs for fiscal 2026. Nike (NKE

This is particularly the case given that the aforementioned weakness in the consumer means that these companies have limited capacity to pass on these increased costs to the consumer via higher prices. Another cause for concern is how much management has been obsessing over the impact of tariffs. This is evidenced in the fact that the mention of tariffs on earnings calls has surged 190%, while the mention of hiring freezes on earnings calls has jumped 286%. General references to “uncertainty” rose by 49%, especially in the industrial and consumer sectors. This reflects management teams that are becoming increasingly cautious and therefore are likely to behave more conservatively, including reducing buybacks and dividend increases in an attempt to conserve cash and preserve their financial positioning through a period of prolonged uncertainty and potential economic weakness. While this study was done on Q1 earnings calls in the wake of the release of Trump’s “Liberation Day” tariffs, such sentiment impacted company actions over the course of the remainder of 2025 and contributed to their underperformance in the stock market. Additionally, some of this uncertainty still persists today.

Why Dividend Growth is Slowing

Additionally, inflation is providing a headwind for these companies because not only is it increasing some of their input costs through higher labor, materials, and production inputs, but also it has stretched consumers thin by giving them less purchasing power, which in turn is driving them towards lower-cost private label products and discount retailers. Therefore, brand loyalty is beginning to crack under pricing pressure.

This produces a vicious cycle where tariffs raise input costs as well as inflation, and then inflation and tariffs also limit pricing power due to a stretched consumer. This, in turn, leads to compressing margins, which then leads to slower dividend growth, and ultimately stock price valuations reprice lower as a result of the slower growth.

Therefore, just because a stock’s yield is rising, for example, as we see with Clorox (CLX

Investor Takeaway

Ultimately, what this means for me is that I am not buying any high-yielding dividend growth stock simply because it has a strong history and today offers a high yield. Instead, I’m primarily focusing on the dividend growth names that are somewhat insulated from these aforementioned headwinds yet still offer a very attractive valuation.

That’s why I like a lot of infrastructure (UTF

Additionally, I like certain REIT (VNQ

That being said, I am still certainly looking at some of these consumer staples dividend growth stalwarts, and I have several on my watch list at the moment, including CAG and UPS. For more on the CAG opportunity, check out my recent analysis here.

If their underlying fundamentals show signs of improvement, and the market does not seem to fully appreciate that, and/or their stocks get cheap enough at a certain point, I will pull the trigger on them.

But for now, I’m steering clear in favor of other very attractive opportunities that have much more promising underlying fundamentals in the current environment in my portfolios at High Yield Investor.

Illustration by Space Stock on Unsplash