Summary

- Outside of commodities and the U.S. dollar, investors are struggling to generate positive total returns in 2022.

- Year-to-date, WisdomTree High Dividend strategies outperformed comparable cap-weighted indexes by over 1000 basis points in developed and over 600 basis points in emerging markets.

- In emerging markets, WisdomTree’s high dividend approach has led to an annualized total return advantage of 9.4% per year over non-dividend payers in the MSCI Emerging Markets Index.

If there was only one global investment theme over the last five years, it was a focus on technology and consumer discretionary sectors. Not having meaningful exposure to tech or the consumer almost guaranteed underperformance versus the benchmark over that period.

In 2022, the theme that is emerging around the world is not simply value versus growth, but rather dividend versus non-dividend payers.

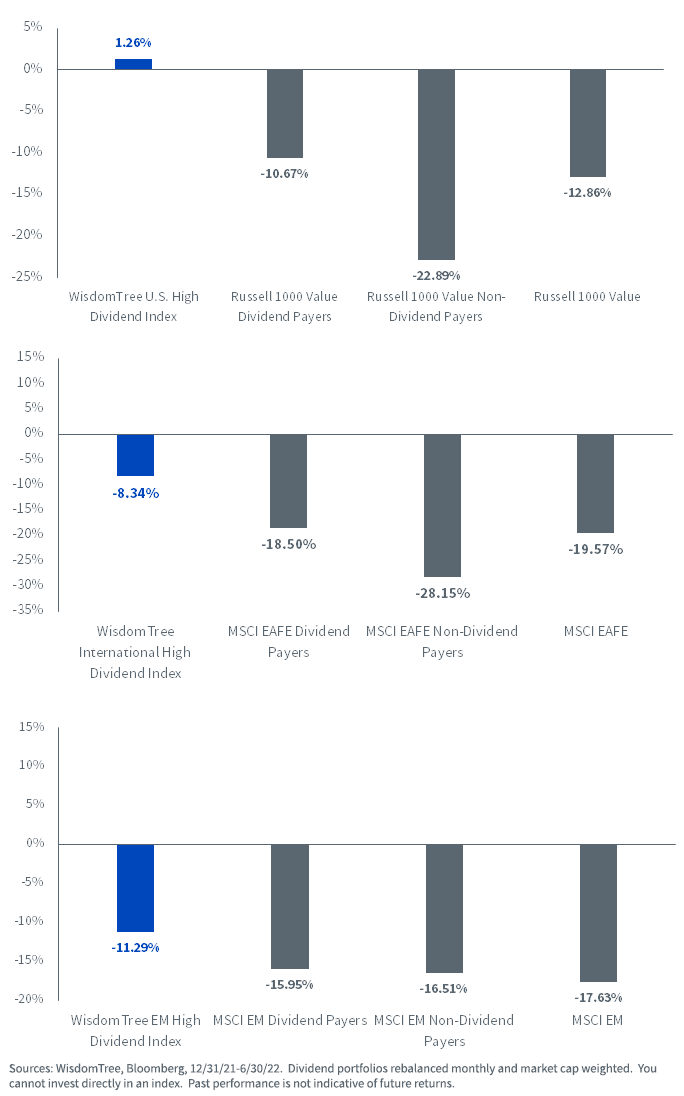

Outside of commodities and the U.S. dollar, investors are struggling to generate positive total returns in 2022. As of June 30, the U.S. market is down 19.96%. International and emerging markets are trailing closely behind with negative returns of 19.57% and 17.63%, as represented by the MSCI EAFE and MSCI Emerging Markets Indexes. While many attribute this to a shift from growth to value, focusing on dividend payers rather than non-dividend payers actually generated even higher returns, even within the value segment.

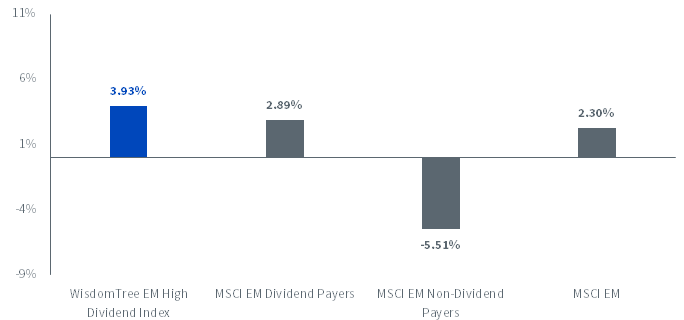

Year-to-Date Returns, as of 6/30/22

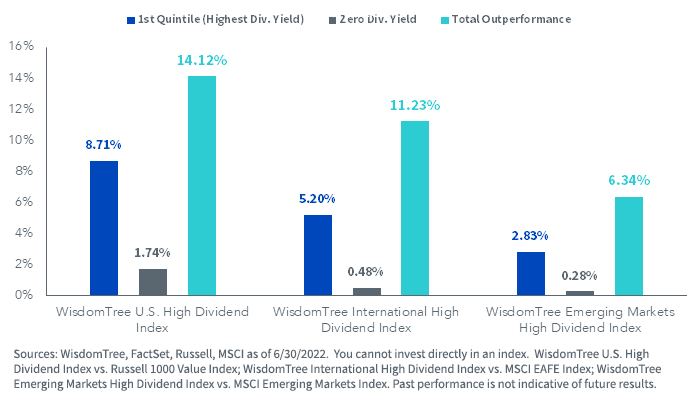

Year-to-Date Attribution

Year-to-date, WisdomTree High Dividend strategies outperformed comparable cap-weighted indexes by over 1000 basis points in developed and over 600 basis points in emerging markets.

- WisdomTree strategies had approximately two-thirds of their portfolio weight allocated to the top dividend yield quintile versus less than 20% for the market cap-weighted indexes, a significant differential.

- An underweight allocation to the non-dividend paying segment of the market was another large contributor to performance. Cap-weighted indexes allocated from 5% to 16% to this segment. In contrast, WisdomTree Indexes allocated less than 1%, as our strategies only include dividend payers at annual reconstitution.

Put another way, allocating to dividend payers has dampened volatility and resulted in higher total returns in both developed and emerging markets. In addition to adding value by what you own, you also added value by what you didn’t own.

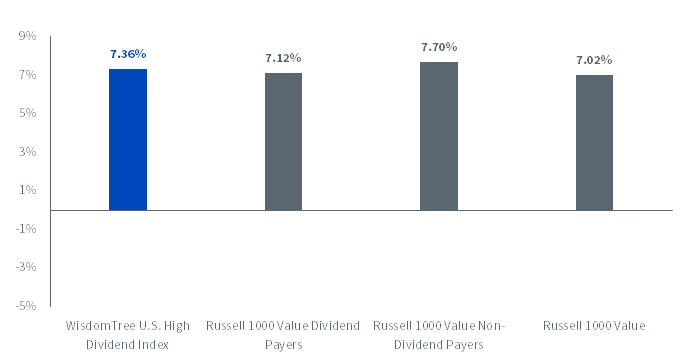

While it may be easy to pass this off as a short-term fad, what’s interesting is that we are starting to see a rotation in longer-term U.S. performance as well. While there has been a wider dispersion among non-dividend payers in broad-market cap-weighted indexes, we are also starting to see a more marked shift among the value segment. In the chart below, we show that since inception, non-dividend payers have historically outperformed. However, we think that this may be an area of opportunity as investors think about the characteristics they are looking for in value.

Since-Inception Returns, as of 6/30/22

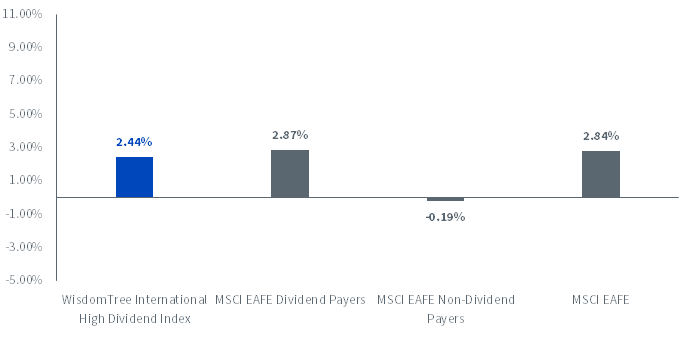

Outside the U.S., a higher percentage of companies tend to pay dividends. By focusing on the highest-yielding segments of the market, meaningful performance can be added relative to cap-weighted peers.

In emerging markets, WisdomTree’s high dividend approach has led to an annualized total return advantage of 9.4% per year over non-dividend payers in the MSCI Emerging Markets Index.

Conclusion

In sum, allocations to tech and consumer discretionary became the key differentiator in total returns over the last five years. As the market continues to look for global catalysts, we believe the rotation to value is still in its early days. Among this value rotation, we believe focusing on high dividends as opposed to low price-to-book may yield higher excess returns versus the market going forward.

Photo by Markus Winkler on Unsplash